Introduction

Financial services are all set to enter an era defined by assembly rather than construction. Instead of building products from scratch, banks and FinTechs would assemble financial experiences using APIs, microservices, third-party platforms, and reusable digital components.

But most organizations underestimate what they are actually assembling. They are not just assembling features – they are assembling decisions, policies, and financial risk across multiple systems.

As a result, it will be possible to combine payments, lending, onboarding, identity verification, and analytics rapidly to launch new offerings.

This composable approach promises speed, flexibility, and innovation. Organizations can introduce products faster, respond to market shifts, and experiment without rebuilding entire systems.

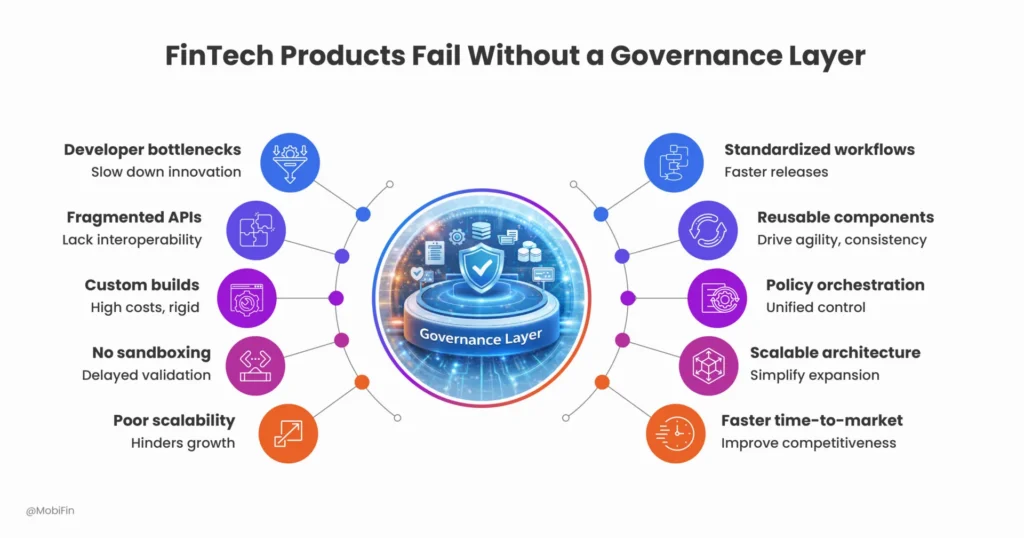

Yet many assembled FinTech products fail to scale beyond initial deployment. They launch successfully. Early adoption looks promising. But over time, operational friction emerges. There are compliance gaps, workflow fragmentation, and lagging of risk controls. Product teams find it difficult to maintain consistency across expanding ecosystems.

The underlying issue is rarely technology capability. Instead, it is the absence of a governance layer.

Composable FinTech accelerates product creation, but without governance, it also accelerates complexity.

The rise of assembled financial products

Traditional financial systems were monolithic by necessity. Product launches required extensive development cycles because every capability was deeply interconnected. While slow, these systems enforced implicit control through centralized architecture.

Modern FinTech replaced monoliths with modularity. APIs enabled connectivity. Cloud infrastructure improved scalability. Low-code orchestration platforms allowed teams to configure journeys instead of coding them entirely.

As a result, financial products today are often assembled from multiple services:

- Identity verification providers

- Payment processors

- Risk engines

- Lending modules

- Customer engagement platforms

- Analytics systems

This modularity enables rapid innovation. However, it also shifts responsibility. Control no longer resides in a single system but must be coordinated across many moving parts, each introducing its own rules, data models, and decision logic. Without governance, modular flexibility becomes operational fragility.

Speed without structure creates hidden risk

Early-stage FinTech success often prioritizes speed. Teams focus on launching minimum viable products, integrating partners quickly, and achieving market traction.

In the absence of governance, each integration solves an immediate problem but introduces long-term complexity. Different teams configure workflows independently. Data definitions diverge. Approval processes vary between products. Risk rules evolve inconsistently.

Initially, these inconsistencies remain invisible. But as transaction volumes increase, cracks begin to surface.

Transaction limits may differ across channels. Risk decisions taken in onboarding may not align with transaction monitoring. Customer profiles may be interpreted differently across systems. Compliance reporting becomes difficult to reconcile. Customer journeys behave unpredictably across channels. Risk decisions lack auditability. Operational teams rely on manual interventions.

The organization discovers that while products were assembled quickly, they were never structurally aligned. Governance is what transforms assembled components into an operating system rather than a collection of integrations.

Governance is coordination

Governance is often misunderstood as regulatory oversight or policy enforcement. In reality, governance is the mechanism that ensures every component of a financial product operates within defined rules and shared logic.

A governance layer defines:

- How decisions are made

- Who controls workflow changes

- How risk policies propagate across products

- How data flows consistently between systems

- How accountability is maintained at scale

At its core, a governance layer brings together policy consistency, decision control, system-wide visibility, and the ability to adapt rules without breaking workflows.

In composable FinTech environments, governance acts as the connective intelligence between services.

Without it, each module behaves correctly in isolation but unpredictably in combination.

The fragmentation problem in composable architectures

Composable architectures distribute responsibility across services. While this improves flexibility, it also introduces fragmentation risks. When onboarding, payments, and lending journeys are configured separately, user experiences diverge. Approval paths differ, escalation rules vary, and operational teams struggle to maintain consistency.

Different systems interpret customer or transaction data differently, often creating multiple representations of the same customer and leading to conflicting decisions. Without governance, analytics lose reliability, and personalization becomes inaccurate.

Risk policies implemented independently across modules create exposure. Fraud controls may exist in payments but not onboarding. Compliance rules may apply inconsistently across regions.

Teams lose clarity over who governs change. Product teams optimize experience, compliance teams enforce policies, and operations teams manage exceptions — often without shared visibility.

Governance aligns these dimensions into a unified operational framework.

Why scaling amplifies governance gaps

A FinTech product may operate successfully with thousands of users even without structured governance. Problems typically emerge during scale.

Growth introduces new variables such as expansion into multiple markets, additional partners and integrations, higher transaction volumes, regulatory scrutiny, and complex agent or merchant ecosystems.

Every new dimension multiplies operational dependencies.

Without governance, organizations experience “scale shock”. Consequently, growth increases operational risk faster than control mechanisms evolve.

Processes that once worked informally become unsustainable. Manual oversight fails. Decision latency increases. Innovation slows as teams attempt to manage accumulated complexity.

Most composable FinTech products do not fail at launch. They fail at the point where scale exposes the absence of coordinated control.

Ironically, the same composability designed to accelerate innovation begins to hinder it.

Governance as an innovation enabler

Contrary to common perception, governance does not slow innovation. Properly designed governance accelerates sustainable experimentation.

A governance layer allows organizations to introduce new products using predefined control frameworks. They can reuse approved workflows and risk logic. It also facilitates maintaining compliance automatically across variations. Ultimately, teams can innovate within safe operational boundaries.

Instead of rebuilding policies for every launch, governance turns compliance and risk controls into reusable assets. Innovation becomes configuration-driven rather than approval-driven.

The core components of a governance layer

Effective governance in assembled FinTech products typically includes several foundational capabilities.

Policy orchestration

Rules governing onboarding, transactions, and approvals must be centrally defined yet dynamically applied across journeys. Policy orchestration ensures consistency regardless of product variation.

Role-based control and hierarchies

As ecosystems expand, governance must define supervisory hierarchies and access permissions clearly. This prevents unauthorized actions while enabling distributed operations.

Auditability and traceability

Every decision within a financial workflow must be explainable. Governance ensures that actions, approvals, and rule changes are recorded and traceable. Auditability reduces regulatory risk while improving operational accountability.

Data governance

Standardized data models and controlled data flows enable accurate analytics, personalization, and reporting.

Without this layer, intelligence systems operate on fragmented information.

Continuous feedback loops

Governance frameworks must evolve through real-time insights. Performance metrics, risk signals, and behavioral patterns should inform automated adjustments.

Governance becomes adaptive rather than static.

Governance in the age of AI and automation

As FinTech platforms increasingly incorporate AI-driven decisioning, governance becomes even more critical.

AI systems learn from data patterns, but without governance:

- Decision logic may drift unpredictably.

- Bias risks increase.

- Regulatory explainability becomes difficult.

In AI-driven environments, governance is not just about control – it is about ensuring that automated decisions remain bounded, explainable, and aligned with institutional risk appetite.

Governance ensures AI operates within defined ethical, regulatory, and operational boundaries.

In this context, governance becomes the guardrail that allows automation to scale safely.

From product thinking to operating model thinking

Many FinTech organizations still approach innovation through product thinking — focusing on features and user interfaces.

However, sustainable success requires operating model thinking.

An operating model defines how product, risk, governance, and growth interact continuously. Governance is the structural backbone of this model, ensuring alignment between innovation and control.

Organizations that shift toward operating-model design achieve several advantages:

- Faster product iteration without compliance delays

- Reduced operational overhead

- Predictable scalability

- Stronger stakeholder trust

Governance transforms growth from reactive management into intentional design.

The strategic cost of ignoring governance

The absence of governance rarely causes immediate failure. Instead, it creates cumulative friction.

Over time, organizations experience:

- Increasing compliance remediation costs

- Slower product launches due to manual reviews

- Operational inefficiencies

- Customer trust erosion after service disruptions

- Difficulty in integrating new partners

Eventually, teams must pause innovation to restructure foundational systems — a far more expensive process than embedding governance from the start.

Governance is therefore not an operational expense; it is a strategic investment.

Building governance into composable FinTech platforms

Modern FinTech platforms must treat governance as a native capability rather than an external layer added later.

This means governance should be:

- Configurable rather than hard-coded

- Embedded within orchestration workflows

- Visible across organizational roles

- Scalable across ecosystems

- Adaptive through data intelligence

Platforms designed with governance at their core allow organizations to assemble products confidently, knowing operational integrity will remain intact as complexity grows. This is where orchestration-led approaches introduce a structural advantage as they ensure that governance is not enforced after composition, but built directly into how workflows are defined and executed.

The future of FinTech assembly

Composable FinTech will continue reshaping financial innovation. Products will increasingly be assembled dynamically, personalized continuously, and distributed across diverse ecosystems.

In this environment, competitive advantage will not come from access to APIs alone. It will come from the ability to coordinate complexity across these APIs intelligently.

The most successful institutions will not just build faster, but more importantly, they will govern better.

Governance will define which organizations can scale innovation safely and which remain trapped managing unintended consequences of rapid assembly.

Conclusion

Assembled FinTech products promise unprecedented agility. But agility without structure leads to instability.

A governance layer transforms modular technology into coherent financial systems. It aligns decisions, enforces consistency, enables trust, and ensures innovation compounds rather than fragments.

In the next phase of FinTech evolution, governance will no longer be viewed as a constraint. It will be recognized as the invisible infrastructure that makes composable finance sustainable.

Financial products may be assembled from components, but lasting platforms are built on governance.

Looking forward to learning more about how Tapestry enables FinTech product composition, and how AI is playing a part in it?

Book a demo Now