Digital banking adoption across Africa continues to expand across retail banking, agency banking, merchant payments, mobile financial services, and government-led financial inclusion initiatives. Financial institutions are under increasing pressure to support larger customer bases, rising transaction volumes, and broader service accessibility across urban and rural markets.

Many banks and financial service providers have introduced digital channels over time, but the underlying infrastructure supporting these services often remains fragmented. Mobile banking, USSD services, payments, onboarding systems, merchant management, and agency banking operations frequently operate across disconnected environments. As institutions scale, these gaps begin affecting operational efficiency, integration timelines, customer experience consistency, and long-term scalability.

Building sustainable digital banking operations now requires platform-based infrastructure that can support interoperability, ecosystem connectivity, transaction scalability, and multi-channel service delivery within a unified operational framework.

Digital Banking Growth Across Africa

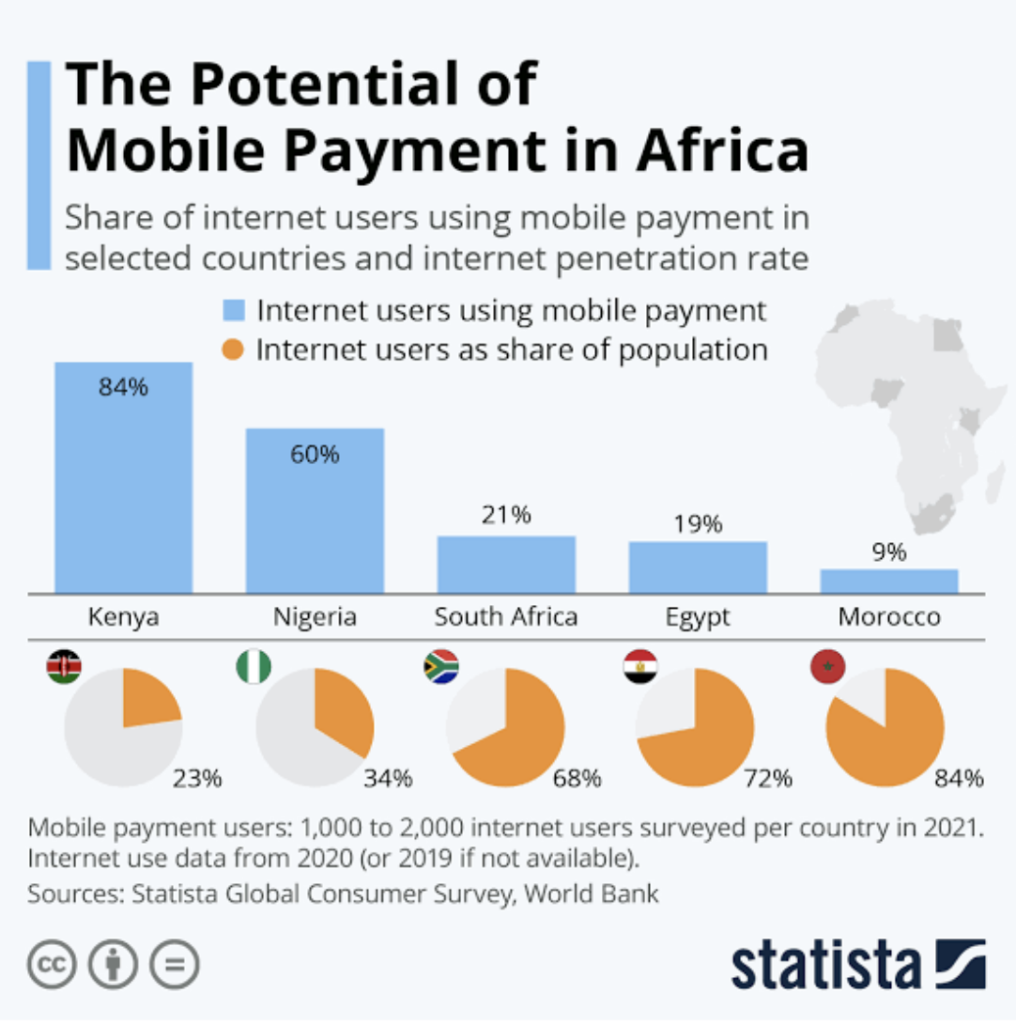

Digital financial services have become central to banking expansion strategies across several African markets. Mobile-first banking behavior, increasing smartphone penetration, and broader internet access are changing how customers interact with financial institutions. Africa continues to lead global mobile money adoption, accounting for more than 70% of the world’s mobile money transaction value according to the GSMA State of the Industry Report on Mobile Money 2024. This growth is increasing demand for scalable digital banking infrastructure capable of supporting wallets, agent networks, merchant ecosystems, and interoperable financial services across diverse markets.

Banking services are no longer limited to branch-led engagement. Customers expect access to onboarding, payments, transfers, merchant transactions, and account management through mobile applications, USSD channels, agency networks, and digital payment ecosystems.

This shift has increased the importance of scalable digital banking platforms capable of supporting multiple customer touchpoints simultaneously. Financial institutions are now expected to deliver consistent service experiences across channels while maintaining operational visibility and regulatory compliance.

As digital ecosystems expand, platform limitations become more visible. Institutions operating on disconnected systems often face delays in launching services, integrating external partners, and scaling operations efficiently across markets.

Challenges with Legacy Banking Infrastructure

Many financial institutions continue to rely on legacy banking environments that were originally designed for limited channel operations and lower transaction complexity. Over time, new digital services are added independently, resulting in operational silos across departments and customer journeys.

These fragmented architectures create challenges in several areas. Customer data becomes distributed across systems, operational reporting lacks centralization, and integration projects require longer implementation cycles. Product launches become dependent on multiple backend modifications, increasing both operational overhead and technology complexity.

In multi-channel banking environments, disconnected systems also create inconsistencies between customer experiences across mobile banking, agency banking, internet banking, and merchant payment platforms.

As transaction volumes continue increasing, these infrastructure limitations directly affect scalability, operational efficiency, and service reliability.

Platform-Based Digital Banking Architecture

Modern banking operations require centralized digital platforms capable of supporting multiple financial services through a unified infrastructure layer. Platform-based architecture enables institutions to manage customer onboarding, payments, wallets, merchant ecosystems, agency banking, loan services, and digital transactions within a connected operational environment.

This approach reduces dependency on isolated systems and allows institutions to scale services more efficiently. Instead of rebuilding integrations for every new product or channel, institutions can extend services through reusable infrastructure components and standardized APIs.

For African financial institutions, platform flexibility is particularly important because banking services often need to operate across varying connectivity environments, customer segments, and regulatory frameworks. A unified digital banking platform improves operational consistency while simplifying ecosystem expansion.

Multi-Channel Banking and Financial Inclusion

Digital banking growth across Africa depends heavily on multi-channel accessibility. Large customer segments continue to rely on USSD banking, agent-assisted transactions, and merchant-led financial services alongside smartphone applications.

Financial institutions therefore require platforms capable of supporting mobile apps, USSD channels, agency banking operations, merchant ecosystems, and digital payments within a single framework. Managing these channels independently increases operational fragmentation and creates additional maintenance overhead.

Integrated multi-channel platforms allow institutions to maintain consistent customer journeys across banking touchpoints while improving operational monitoring and transaction visibility.

This becomes especially important in financial inclusion initiatives where accessibility, transaction reliability, and low-connectivity support directly influence service adoption.

Interoperability and Ecosystem Integration

Banking infrastructure across Africa increasingly depends on ecosystem connectivity. Financial institutions now interact with mobile money operators, FinTech providers, payment switches, identity verification systems, telecom networks, and government platforms.

Traditional banking infrastructure often struggles to support this level of interoperability because integrations were not originally designed for open ecosystem participation. As partnership requirements increase, integration complexity becomes a significant operational challenge.

Digital banking platforms designed around API-driven architectures simplify ecosystem connectivity by enabling institutions to integrate external services through standardized frameworks. This reduces deployment timelines while improving scalability across payment ecosystems and digital financial services.

Interoperability also allows financial institutions to introduce new services more efficiently without creating additional infrastructure silos.

Agency Banking Infrastructure

Agency banking remains one of the most important financial access channels across several African markets. Expanding agent networks allows financial institutions to extend services beyond traditional branch infrastructure while improving accessibility in underserved regions.

However, scaling agency banking operations requires centralized operational control across liquidity management, agent onboarding, transaction monitoring, commissions, settlements, and fraud management.

Institutions operating fragmented systems often encounter visibility challenges as agent networks grow. Operational reporting becomes delayed, reconciliation processes become more complex, and customer service consistency becomes harder to maintain.

Digital banking platforms designed for agency banking environments provide institutions with centralized management capabilities across distributed networks. Real-time transaction visibility, agent performance monitoring, and integrated operational controls become essential as agency ecosystems expand.

Scalability and Operational Efficiency

Scalability requirements continue increasing as institutions expand customer bases, transaction volumes, and partner ecosystems. Infrastructure decisions made during early digital transformation phases often determine how efficiently institutions can scale over time.

Platforms designed with modular architecture allow institutions to introduce services incrementally without repeatedly restructuring backend operations. This reduces operational disruption while supporting long-term expansion across products, channels, and markets.

Operational efficiency also improves when institutions consolidate reporting, transaction management, customer data, and ecosystem integrations within unified digital infrastructure. Centralized visibility enables faster decision-making while reducing operational duplication across systems.

As digital banking adoption accelerates, scalability can no longer be treated as a future infrastructure consideration. It directly affects service continuity, operational performance, and institutional growth capacity.

Security, Compliance, and Operational Governance

Digital banking expansion increases the importance of platform-level security and regulatory compliance. Financial institutions are expected to maintain secure transaction environments while supporting higher transaction volumes and broader ecosystem participation.

Security frameworks must support authentication controls, transaction monitoring, role- based permissions, fraud management, audit visibility, and regulatory reporting requirements across all banking channels.

Compliance requirements also continue evolving as regulators strengthen oversight across digital financial services, payments, and customer protection frameworks.

Embedding security and governance controls within platform architecture improves operational resilience while reducing compliance complexity across distributed banking environments.

Conclusion

Digital banking growth across Africa is increasing the need for scalable, interoperable, and multi-channel banking infrastructure. Financial institutions are expected to support broader service accessibility while managing growing operational complexity across payments, onboarding, agency banking, and ecosystem integrations.

Fragmented digital environments limit scalability and create operational inefficiencies that become more difficult to manage as institutions expand. Platform-based digital banking architecture provides a more sustainable foundation for managing growth across channels, products, and partner ecosystems.

Institutions investing in integrated digital banking infrastructure will be better positioned to support long-term operational scalability, ecosystem connectivity, and financial service accessibility across evolving African banking markets.

MobiFin provides digital banking infrastructure designed to support banks, financial institutions, telecom operators, and FinTech ecosystems across emerging markets.

The platform enables institutions to manage mobile banking, agency banking, merchant ecosystems, digital onboarding, payments, wallets, and financial services through integrated digital infrastructure. Its modular architecture supports interoperability, scalability, and multi-channel service delivery across diverse operational environments.

By consolidating digital banking operations within a unified platform framework, financial institutions can reduce infrastructure fragmentation while improving operational visibility, ecosystem integration, and service scalability.